Reinforcement Learning for Bond Allocation in Global Pension Fund Portfolios

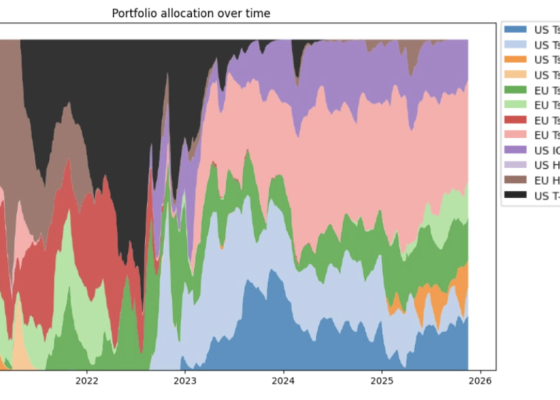

In this project, supervised by Tredje AP-fonden (AP3), the analysts Edvin Gunnarsson, Victor Mikkelsen and Carolina Oker-Blom explore whether Reinforcement Learning (RL) can optimize global bond allocations by dynamically balancing duration and credit risk. Using the Proximal Policy Optimization (PPO) algorithm combined with PCA-based dimensionality reduction, they develop an agent designed to adapt to shifting market regimes and complex macroeconomic conditions.