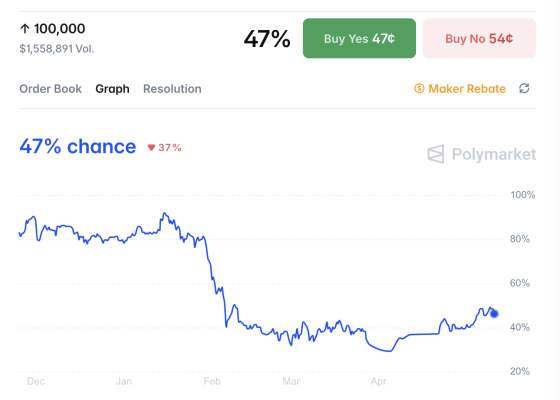

In this project, analysts Carl Nordahl, Alexander Ihrfelt and Alfred Hultgren investigate whether crypto prediction market contracts can be valued using traditional derivatives pricing methods. Focusing on Polymarket contracts tied to the question “What price will Bitcoin hit in 2025?“, they model the contracts as one-touch barrier options and compare a closed-form approximation with a Monte Carlo framework using EWMA volatility and jump-diffusion dynamics.

The analysis finds that both models explain a substantial share of Polymarket price movements, suggesting that prediction market prices reflect economically meaningful probability assessments rather than pure sentiment. However, the Monte Carlo approach performs more consistently across barrier levels and longer horizons, particularly when jump risk is included. Delta-hedging tests further show that model-implied hedge ratios can materially reduce P&L variance, supporting the view that crypto prediction markets can be analyzed with many of the same tools used in traditional derivatives markets.