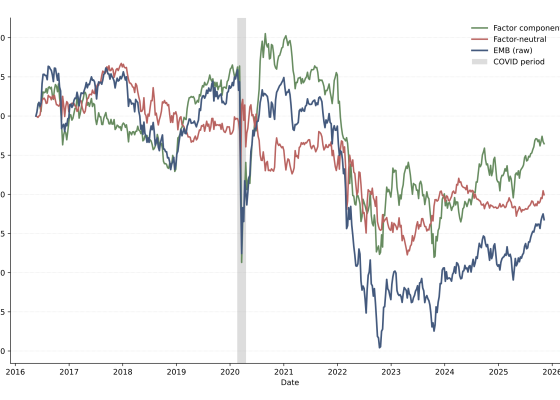

In this project, supervised by OQAM, analysts Vilhelm Hilding, Jacob Fransson and Dag Vallien investigate how global macro conditions drive the returns of two emerging market bond ETFs: EMB (USD-denominated) and EMLC (local-currency). Using a rolling linear factor model, they estimate time-varying exposures to equity markets, US dollar strength, interest rates, credit sentiment, commodities, and volatility across a 10-year period.

The analysis finds that factor exposures are regime-dependent rather than stable, with EMB primarily driven by interest rate and equity conditions while EMLC is dominated by US dollar strength, reflecting its structural sensitivity to currency dynamics. Spread analysis further reveals that the relative performance of EMB versus EMLC varies systematically across regimes, with EMB outperforming during risk-on environments and EMLC narrowing the gap in risk-off periods.