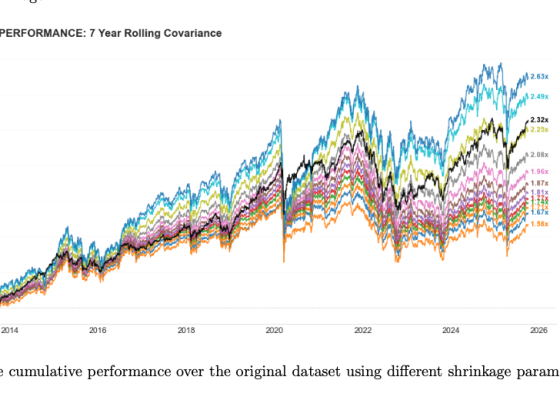

In this project, supervised by AP3, analysts Alexander Nilsson, Peder Persson, and Samuel Eriksson investigate whether Mean-Variance Optimization (MVO) can be enhanced by shrinking the off-diagonal elements of the covariance matrix. Utilizing a 20-year dataset, they backtest models incorporating spectral filtering and shrinkage techniques to assess the robustness and practical feasibility of the optimization process.

The analysis finds that while standard MVO often yields unintuitive portfolio allocations, the application of spectral filtering and shrinkage mitigates these issues, leading to superior risk-adjusted performance. However, the findings also indicate that shrinkage can adversely affect tail-risk metrics as the resulting concentration reduces diversification benefits. Consequently, the analysts conclude that these models are possibly better suited for systematic trading strategies than for the traditional mandates of pension fund management.